JLL’s Portugal Real Estate Market Report 2022 / 2023

By Pedro Lancastre CEO JLL

Every year the real estate market has faced challenges and has been able to overcome each one of them. 2022 was no different! Expectations at the beginning of the year were high as the Covid-19 threat seemed to be fading, allowing the return to a “normal” way of living and doing business. Notwithstanding, the Ukraine/Russia conflict, which began in February, affected global commodity markets and trade flows; the energy shock has driven inflation and a cost-of-living crisis for households across Europe; and central banks are raising rates, pushing up borrowing costs and forcing a repricing of risk and return across all asset markets, including real estate.

Against all odds, the real estate market has outperformed in Portugal. This was the year of a new record high in commercial investment surpassing the €3.0B threshold totalling €3.4B, 2% over the previous record in 2018. 80% of this volume continues to be international which is a very positive sign of the market attractiveness for main overseas players. The allocation of capital has also been diverse with the Hotel sector exceeding €1.1B due to the acquisition of Portfolio Crow for €850M by David Kempner. The I&L sector has also been in the spotlight with several transactions and a total allocation above €600M and several great international players involved in the major deals. Shortage of eligible products in core segments like offices is constraining market performance although this is still one of the most attractive segments in Portugal.

JLL’s Real Estate Market highlights 2022 - 2023 Source credit: JLL

The residential market has outpaced its activity and is expected to have reached another record high. The sales volume is forecast to have surpassed 30 thousand million euros with more than 168,000 units sold, anchored on the best first half of the year since there are records. Regardless of the increase in interest rates, the market attractiveness has not faded. Portugal continues to be an attractive living destination for the international market while the domestic one continues to be very vigorous. Nevertheless, the market faces a structural undersupply which is not only creating price upsurges, but also housing accessibility constraints in a part of the population.

The leasing markets have also exceeded the best expectations. In Lisbon, the office takeup reached 272,000 sqm the highest value ever while Porto has maintained its standard absorption rate. Office demand is robust and occupiers are looking for Grade A and sustainable certificated buildings to comply with their ESG policies and guarantee the attraction and retention of talent.

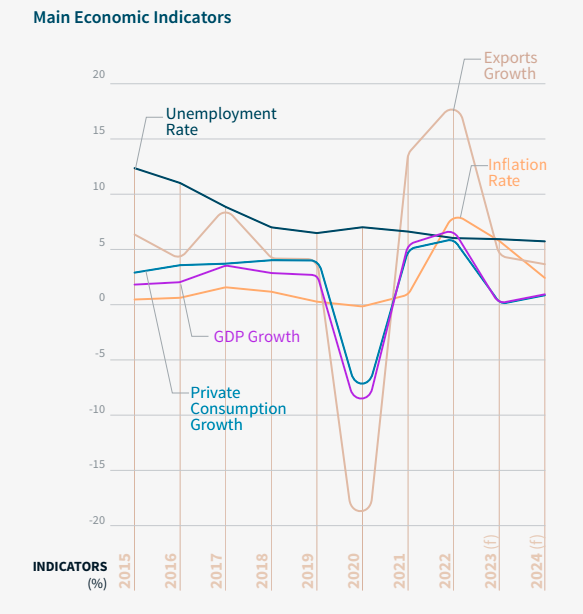

Sources credit: INE, World Bank, Statista via JLL

The I&L market has struggled due to the scarcity of supply. Nevertheless, the total Take-up was c. 560,000 sqm, very positive in the current market framework. First and foremost, Portugal is now on the radar of logistics, and the debut of some international players as well as the consolidation of others that have entered the market recently is a symptom of the market attractiveness.

Last but not least, retail has recovered in 2022 boosted by the tourism sector. The volume of sales is currently at pre-covid levels, the luxury market is expanding in Portugal and the retail parks have been revamped anchored both on retailers and end users’ demand. Rents have also been increasing but the gap between prime and secondary is evident.

Sources credit: Confidencial Imobiliário/SIR, JLL

Despite all setbacks and uncertainty, prospects for 2023 are far from bad. Whilst conditions are harder, there are positive signs as inflation now looks to have peaked, the majority of repricing is underway or will conclude in the first half of the year and recovery looks possible in the second half of the year.

Furthermore, there is a considerable amount of dry powder to be deployed and therefore no systemic risk is perceived. As for Portugal, market fundamentals remain strong and the general scarcity of supply across the real estate spectrum creates great prospects. ESG transition, driven by the recent legislation, is underpinning development and real estate retrofitting, which will create additional opportunities in the market.

The full report can be found here.

Disclaimer: The views expressed above are based on industry reports and related news stories and are for informational purposes only . SSIL does not guarantee the accuracy, legality, completeness, reliability of the information and or for that of subsequent links and shall not be held responsible for any action taken based on the published information.